Whatever you might think of the Republican tax bill from last fall, it has now been passed into law and has already started to affect your income taxes for 2018. In many cases, your tax burden as a graduate student or postdoc will decrease for this year compared to last year, which means you’ll have more money in your pocket starting with your January or February paycheck.

Will Your Take-Home Pay Increase?

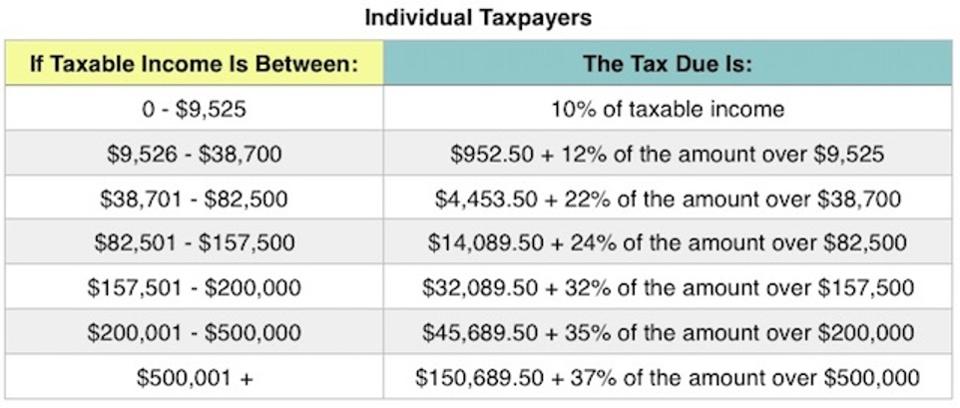

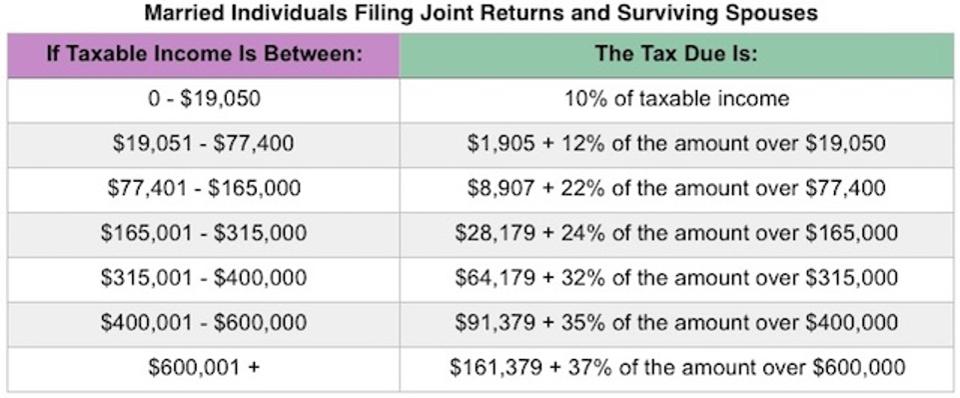

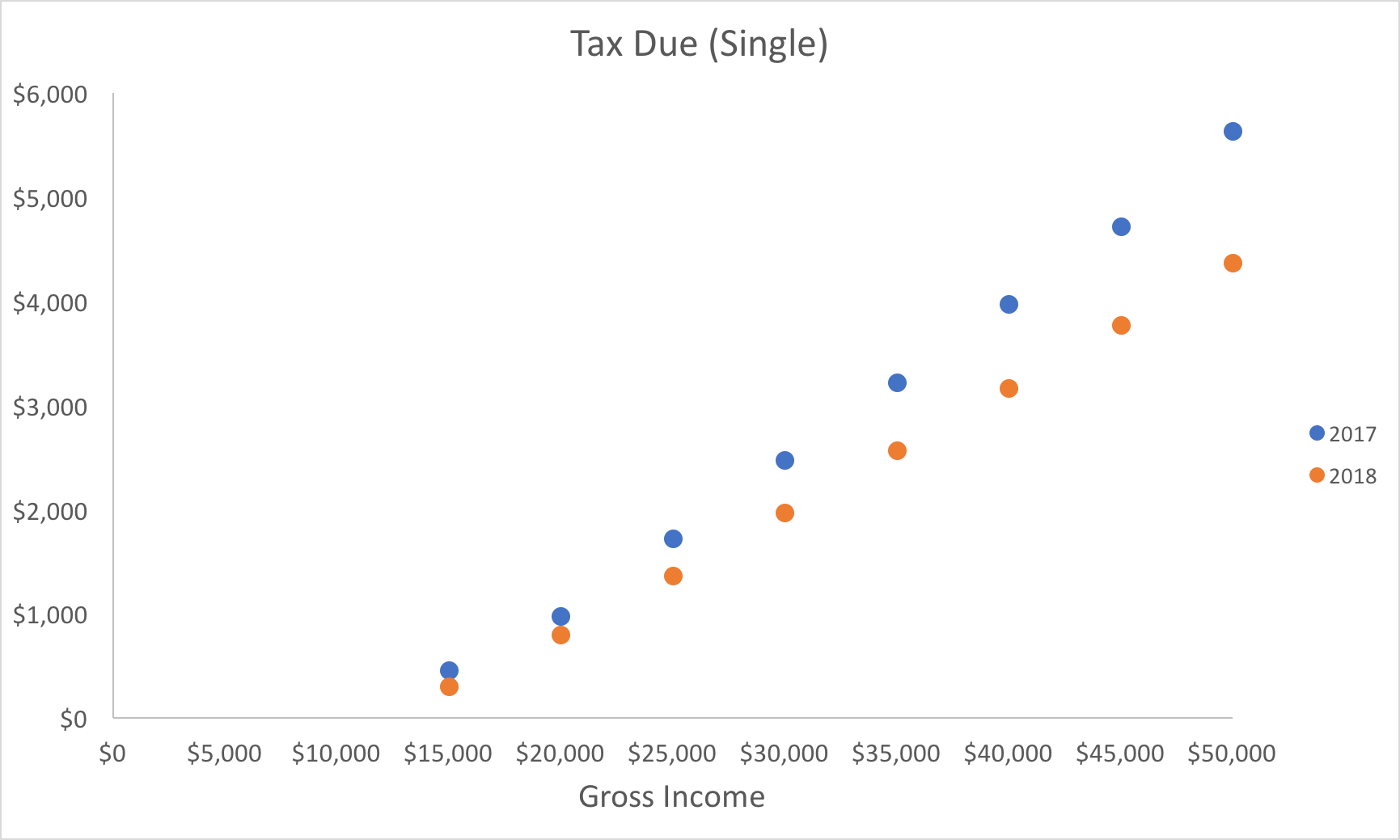

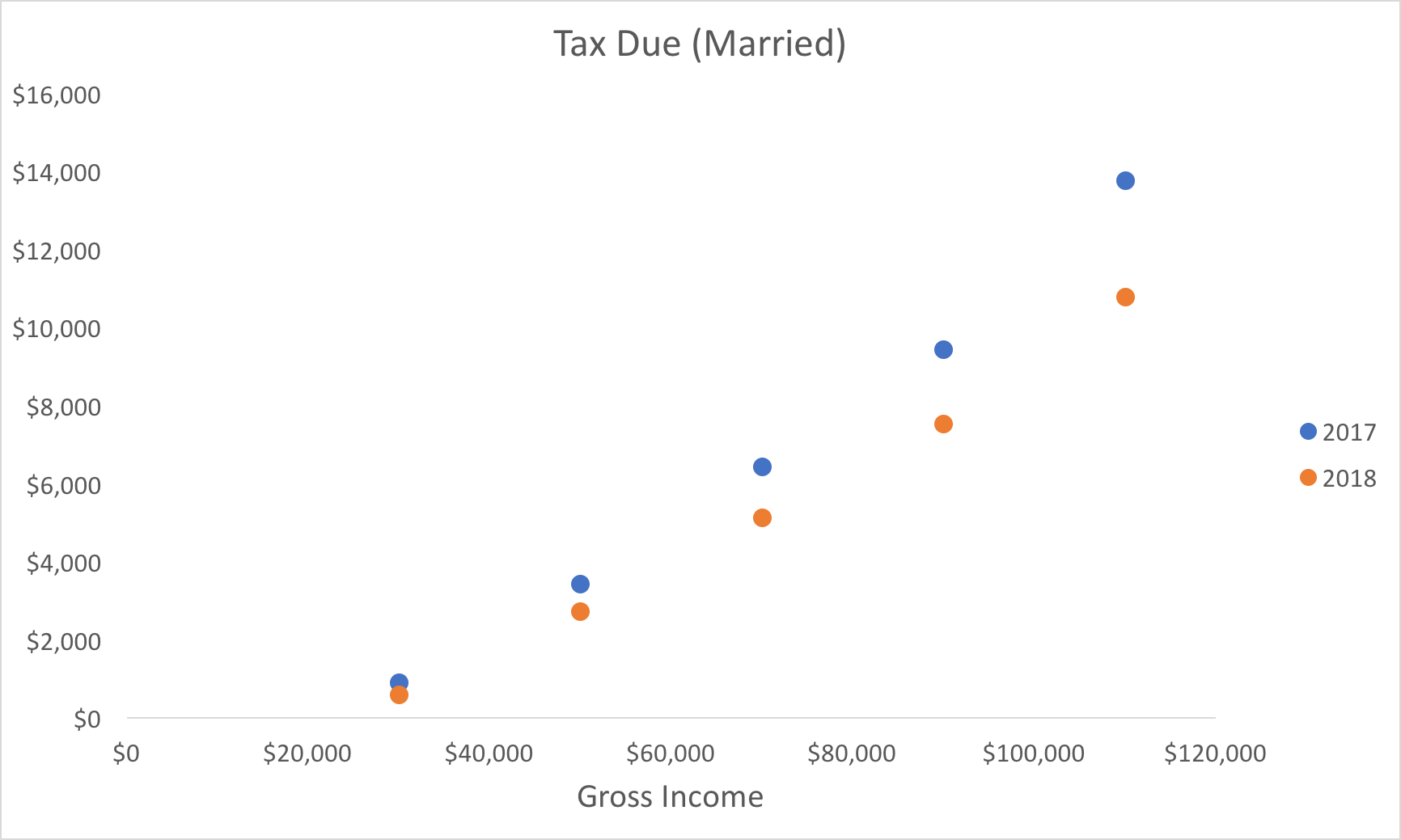

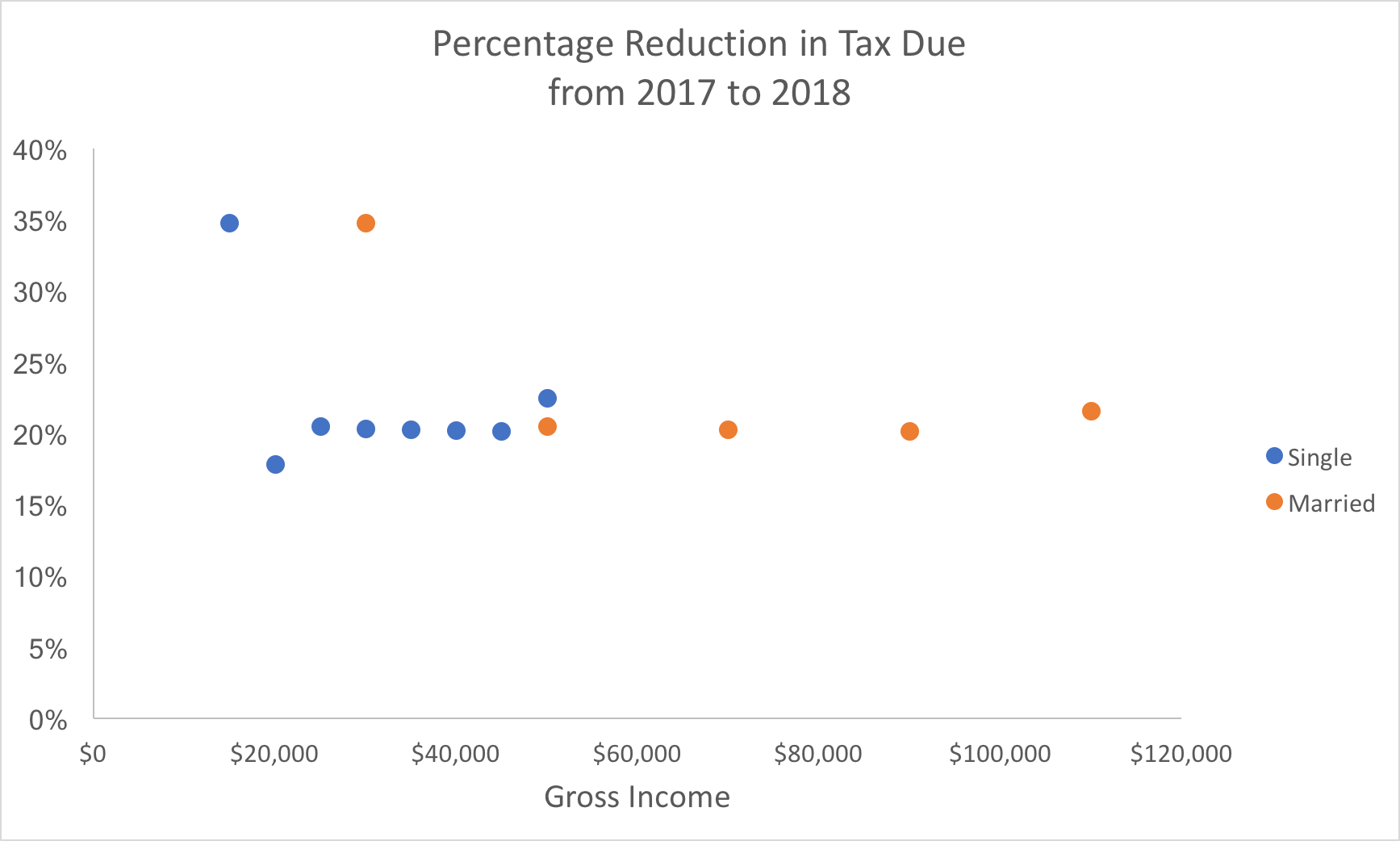

A few weeks ago, I calculated what the tax burden would be for single or married people with no dependents with the income ranges that are most common for graduate students and postdocs ($15,000/year to $110,000/year). I found that across those income ranges, the tax burden decreased by 20-35%. Families with children under the age of 17 would see an even further decrease due to the larger Child Tax Credit.

Download the Tax Spreadsheet

Sign up for our mailing list to receive the spreadsheet I used to write this post, including a 3-question calculator for your own 2018 tax due.

To perform these calculations, I assumed that you will take the standard deduction on both your 2017 and 2018 taxes. If that assumption is true (and your income is in the above range), you should see a decrease in your tax burden.

The taxpayers who may see an increase in tax due under the new law are those who currently itemize their deductions, such as households who have in the past deducted more than $10,000 in property tax and state and local taxes together. Another group that may see a higher tax liability under the bill (depending on the rest of their situation) is parents of dependent children aged 17 and older; the exemptions they used to take have been eliminated, and the expanded child tax credit is only for children up to age 16.

Further Reading:

- How Will Taxes for Grad Students and Postdocs Change Under the New Law?

- Will Your Taxes Go Up or Down in 2018 Under the New Tax Bill?

However, I think my assumptions are valid or at least reasonably accurate for the vast majority of graduate students and postdocs, who tend to be younger with lower incomes/expenditures. It’s safe to say that most graduate students and postdocs will see a higher take-home pay in spring 2018 than they did in fall 2017; effectively, you will see a ‘raise.’

What to Do with Your Income Increase

I have no shortage of ideas of actions you can take with your increased take-home pay, whether it’s $14.50/month (for a single person with no dependents earning $20,000/year) or $109/month (for a married couple with no dependents earning $70,000/year). Chances are, last month you didn’t have a lot of money lying around begging to be put to use, and starting pretty soon you will have some non-spoken-for money to work with.

Don’t let this money just disappear into the ether! Allocate it to something specific. If possible, I recommend you set up an automated transfer from your checking account to wherever the money needs to go so that you relieve your willpower/memory of the responsibility of making the transfer manually.

Financially Responsible Action Items

Add to Your Emergency Fund

If you don’t yet have a dedicated emergency fund with a balance of $1,000 (or a higher target, e.g., three months of expenses), use the extra money to beef up your emergency fund! When (not if!) life throws you a curveball, your emergency fund is what stands between you and serious financial consequences.

Further Reading:

Start Investing/Add to Your Investments

YES it is possible and worthwhile to start investing with just a few dollars per month and it’s also amazing to even incrementally increase your existing regular savings rate!

Using this compound interest calculator to estimate, adding just $25/month to your investments for one year, at an 8% rate of return in 50 years that $300 will become over $13,000! If you kept up that higher savings rate for all 50 years, it becomes over $172,000! Sure, that’s not all the saving/investing you will need to do for your retirement, but even a small regular savings rate helps a lot.

Further reading:

- Why You Should Invest During Grad School

- Are You Read to Invest Your Grad Student Stipend?

- Whether You Save During Grad School Can Have a $1,000,000 Effect on Your Retirement

- Everything You Need to Know about Roth IRAs in Graduate School

Free Email Course: Investing for Early-Career PhDs

Sign up for the mailing list to receive the free 10,000-word email course designed for graduate students, postdocs, and PhDs in their first Real Jobs.

Pay Down Debt

Similar to the investing example, a few extra dollars per month thrown at your existing debt can accelerate your progress to debt freedom.

If you currently had $500 in outstanding credit card debt and were making the minimum payment of $25/month, it would take you 23 months to pay off the card. But if you instead paid $50/month, you would knock out that debt in 11 months!

While you are not required to make payments on deferred student loans, if they are unsubsidized they are currently accruing interest. For example, if you had $10,000 of deferred unsubsidized loans at 6.8% interest and five years until graduation (and the end of the deferment), putting $25/month toward your loans would decrease the $14,036 you would have owed at the end of grad school to $12,255 (the $1,500 you paid decreased your debt by $1,781).

Further reading:

- Options for Paying Down Debt During Grad School

- What Is the Best Way to Pay Down Debt?

- Why Pay Down Your Student Loans in Grad School

Invest in Your Career

Instead of using your money to increase your financial security or net worth directly, you could double down on your PhD training and invest in your career. Not many universities provide adequate career exploration and training for PhD students and postdocs, especially for “alternative careers.” You could use your increased cash flow to save up to attend a key conference in your field (if you’ve already used the funding available to you) or for a career path you’d like to get into. You could join a membership site like Beyond the Professoriate to help you transition out of grad school/your postdoc/your current job and into a fulfilling job. You could take a one-time seminar on negotiating a job offer; think of the ROI on that training!

Not-Financially-Focused-But-Still-Good Ideas

There are plenty of good ideas of what to do with money that will have a positive impact on your well-being rather than your bottom line specifically.

Treat Yo Self

Set aside a bit of time to consider what would give you the most ‘bang for your buck’ with this extra cash flow in terms of increasing your satisfaction in your life. You could use it on a monthly basis to take a fancy exercise class, have a special date night, enroll in a new subscription service, or care for a small pet. You could save up over the course of a few months or the year and take an extra flight to see loved ones, purchase new electronics (my husband is currently eyeing an ergonomic mechanical keyboard!), or update your wardrobe. What will mean the most to you is obviously quite personal, but whatever you choose, the key thing to do is to earmark the extra money for your choice so that it doesn’t get swept up in the rest of your expenses.

Give

At any point in 2017 or earlier, did you come across a non-profit or certain cause that you had the impulse to donate to, but you just didn’t have the available funds? This is your opportunity! You can now set up a recurring donation to a group whose work is meaningful to you. Non-profits really appreciate steady contributions that they can plan on. Alternatively, you could set aside a dedicated savings account with a monthly automatic savings rate that is earmarked for giving. My husband and I did this in graduate school for one-off donations that we would make a few times a year, and it was a wonderful feeling to be able to say “yes” when an opportunity presented itself without having to scramble or make hasty calculations.

Don’t let this opportunity to act intentionally with your increased cash flow pass you by! It might be quite a while before you get another increase in your take-home pay so make the most of it.