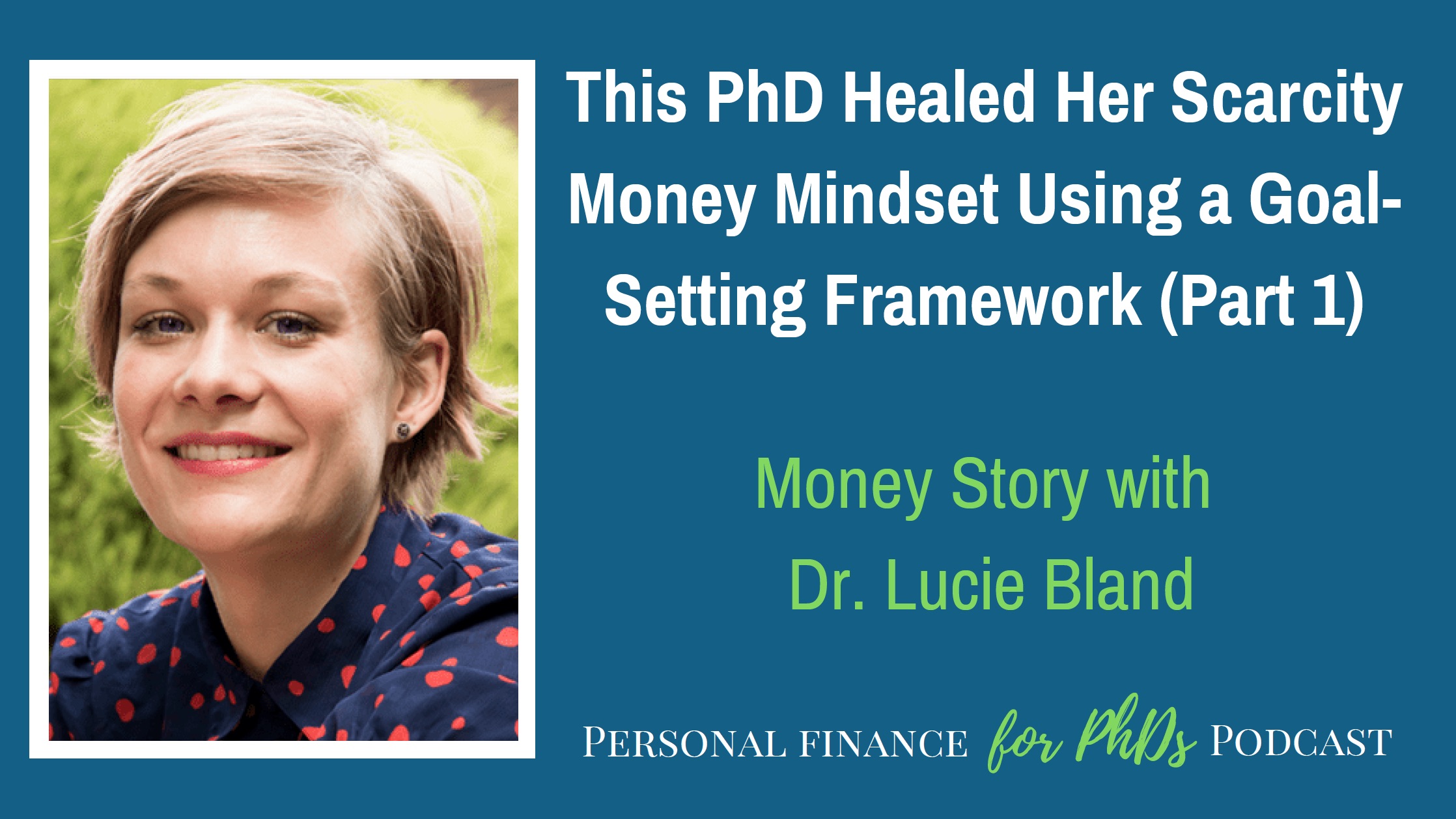

In this episode, Emily interviews Dr. Lucie Bland about her financial journey from graduate school to self-employment. Lucie was severely underpaid as a PhD student, and she felt such guilt and shame around spending that she became terrified of money. Her money mindset didn’t improve when her income increased several-fold as a postdoc, and it wasn’t until she discovered the Good-Better-Best goal setting framework that she started to heal her relationship with money. She now describes herself as a money boss. In this first half of the conversation, Lucie details her financial journey from underpaid PhD student to well-paid postdoc and how she needed to take a break from full-time employment to set herself on the right career and financial trajectory.

Listen to Part 2 of this interview!

Links Mentioned in the Episode

- Lucie’s Website: luciebland.com

- Personal Finance for PhDs: Speaking

- What Color is Your Parachute?

- Good-Better-Best with Megan Hale

- Financially Navigating Your Upcoming PhD Career Transition

- Personal Finance for PhDs: Help Out

Teaser

00:00 Lucie: I did go to some extent through that transition of seeing not money as like an enemy or something that needs to be hoarded, but something that can be used as an investment for a good life. When I was doing my PhD, I was not future-oriented. I was in survival mode.

Introduction

00:21 Emily: Welcome to the Personal Finance for PhDs podcast, a higher education in personal finance. I’m your host, Dr. Emily Roberts. This is season four, episode five, and today my guest is Dr. Lucie Bland, self-employed PhD living in Australia. Lucie has such an amazing story to tell that I’ve split it into two episodes. This one and next week’s. In this episode, Lucie talks us through the roller coaster of her financial journey from severely underpaid graduate student in London to well-compensated postdoc in Australia to not having an income to starting a business. Lucie describes herself during graduate school as “terrified of money,” And that didn’t automatically improve when her income more than tripled and her cost of living dropped. We discuss the intentional steps she took to heal her money mindset, including the goal-setting framework that she now applies in her personal and professional life. Without further ado, here’s the first part of my interview with Dr. Lucie Bland.

Will You Please Introduce Yourself Further?

01:26 Emily: Thank you so much for joining me on the podcast today. We have a really delightful set of episodes ahead for us. It’s going to be a two-parter. My guest today is Dr. Lucie Bland and so I’m going to kick it right over to her right now and have her introduce herself to you a little bit further.

01:44 Lucie: Thank you, Emily. Thank you for having me on the podcast. My name is Dr. Lucie Bland. I’m an editor and writing coach and I help researchers and writers get published.

01:54 Emily: Yeah, that sounds really exciting. Can you tell us what your background is?

01:59 Lucie: Yeah. I graduated from Oxford University with a degree in biological sciences and then I did my PhD at Imperial College, London in Ecology in 2014. That’s when I finished, and then I moved to Australia for two postdocs in conservation science. The first one at the University of Melbourne and the second one at Deakin University. And now for about a year I’ve been running my academic editing business, which I now do full time. So very much serving the academic community, but I’m no longer directly a researcher.

02:34 Emily: Yeah. Well, we are in the same boat in that respect. Can you say right away up top what your website is?

02:42 Lucie: My website is luciebland.com and that’s spelled l u c i e b l a n d.com.

02:49 Emily: Yeah. And any other personal details you’d like to share, maybe where you’re living now or is your household just you?

02:56 Lucie: I live in Melbourne with my boyfriend and our Burmese mountain dog that you might see in the video if he comes around.

03:05 Emily: Yeah. Enticement to hop over to YouTube and watch this on the video instead of over the podcast. Okay. So we have this great story that I know a little bit about already, so bring us back to your time in graduate school. What was going on with you financially at that time, both in terms of like how much money you were making and also what was your relationship with money?

Lucie’s Evolving Relationship to Money

03:30 Lucie: Yeah, my money situation, my relationship to money when I was doing my PhD was very different to how it is now. I was living in London, one of the most expensive cities in the world, and I was earning 13,000 pounds per year, which is 16,000 US dollars. And I would spend 650 pounds a month on rent, which is 60% of my income. And I remember that time reading a report that said that your level of basic socioeconomic level can be determined by how much you spend on rent, and the higher it is the poorer you are. So that was a little bit depressing to me. But despite having these really high expenses and that really low income, I was really not wise about money at all. My money strategy was to bury my head in the sand. I was paid quarterly, which would mean that I would run out of money every quarter.

04:27 Lucie: And I didn’t have a savings account. So normal accounts could be very regularly in the double digits and I just didn’t know how that would happen. And when I moved to Australia, I experienced a very different money situation in that my income pretty much tripled. I was paid $80,000 a year and I lived in a really funky flat on my own in the hipster part of town. So I kind of went from rags to riches, but I very much kept my very Scrooge-y lifestyle and I still didn’t budget. It did mean that I was saving $20,000 a year because my expenses were really low cause I would still collect vouchers and coupons and have that very “PhD student” lifestyle. But I wouldn’t say that my budgeting skills or my approach to money improved in any way. It was just that my income was higher.

05:26 Emily: Gotcha. Yeah, that’s a great overview, and I think it’s one that’s going to be relatable to a lot of people within the audience. Most of my audience is in the U.S. and the cost of living differences can be so wide between, you know, New York and San Francisco versus certain cities in the Midwest that are quite a bit smaller. And so a graduate stipend can also kind of be all over the map and it doesn’t necessarily correlate with higher stipends in higher cities necessarily. Sometimes that’s the case and sometimes not. I’ve interviewed several people on the podcast who live in high cost of living cities but have an okay kind of income, maybe double or more what you just mentioned, and others where that’s completely not the case. A much, much lower income. Actually, I want to go back a little bit further and talk about your mindset from even before you started graduate school. Would you say that you grew up middle class, or what was your mindset about money or the socioeconomic status you had prior to entering graduate school?

Money Mindset Before Grad School

06:34 Lucie: Yes, so I was definitely middle class. Especially my father had a very relaxed and confident approach to money and to some extent my mother as well. But in a way they hadn’t taught me any budgeting skills at all, which is a little bit sad, but kind of looking a bit backwards again. And that has really influenced my money story. My French grandparents grew up under German occupation and under rationing and that really influenced their mindset around money and around the use of resources. And to some extent, even in my kind of middle class nuclear family, especially, my mother could also have that very Scrooge-y or scarcity mindset. And I remember my grandparents still drinking chicory, which is a coffee replacement that’s made from the root of a plant, that French people used to drink under the German occupation.

07:30 Lucie: And so they still had some of these relic habits of, you know, we don’t know when the next meal is coming. And so you’ve got to finish off your plate, you’ve got to use all your resources in a very savvy way, which in many cases can be a good approach. But I think that as a child, I really internalized that. And one of the funny stories in my family is that at the age of 10 or 11, I signed up to this website, it was called scrooge.com and got lots of vouchers and was very obsessed with using those and not spending any money. So, I’m quite conscious that my personal money story and approach to money, well to some extent determined by my socioeconomic level or being from a middle-class family, was also influenced by lots of other family patterns that predated that.

Money Mindset During Grad School

08:20 Emily: Yeah. So I guess we could suffice to say that in some ways you were unprepared for being in graduate school on that kind of income and in that expensive city. In other ways, you had maybe some skills and some mindsets that would be, I hesitate to even say helpful. I mean helpful to survive, but maybe not helpful to be sort of healthy mentally overall towards money, especially later on once you have that income increase. So when you were accepted to graduate school and you knew what that stipend was going to be, and you knew more or less where you’d be living and that it was going to be 60% of your income going towards rent, what were your thoughts? How did you approach that situation? Did you think, “well, I’m just going to have to make this work. I’ll do it somehow”? Or did you consider debt? And I don’t know if that was even really an option for you.

09:14 Lucie: The thing is I didn’t even know that I was going to spend 60% of my income on rent because I hadn’t calculated it at all. I was completely in the dark, and no, that was not an option. I’ve never had a loan or credit card. Again, different countries have different approaches to that. And for me, I was just going to have to eat pasta. That’s how short-sighted my thinking was. To some extent, I could have considered a student loan, which I might not have been eligible for as a French person. But you know, my thinking was not even that advanced.

09:54 Emily: Right. And so once you did find out, once you did secure housing and you knew how much of your stipend was going to be eaten up by rent, what was your plan at that point, and kind of how did you get through it? And I guess this might be sort of advice in sort of how to keep expenses low. Although of course in the overall arc of this conversation, that’s not really what we want to be talking about. But for those years, how did you get by?

10:19 Lucie: I probably spent very little money on food, and I did go out a little bit, but I wouldn’t do anything that was fun. You know, I would probably not go to the cinema. I probably would not go to expensive parties. One of the things I did in London, I had a bike and I would be very savvy about whether I would take the tube or the bus. The bus was cheaper, and so everything became a decision. And if the decision presented itself to me, I would always take the cheaper option. So, I didn’t think long-term about do I need to build savings? Do I need to think a bit longer term? It was extremely short-term.

10:57 Emily: Was thinking long-term even an option though?

Short-Term versus Long-Term Vision

11:01 Lucie: At that stage, I wasn’t thinking long-term at all because I just couldn’t. I didn’t have the funds to do it.

11:09 Emily: Yeah. It’s not really a personal oversight. It’s just this is how the day-to-day is passing by of thinking about these really minute decisions around money, which are so important to whether you’re going to stay in the block for the month or the quarter. So you were surviving by being extremely frugal in many areas and not spending much on entertainment. I wonder, were your classmates living in a similar manner?

11:39 Lucie: Yes. Yes, we were all living in house shares in London. In quite difficult conditions with lots of issues with housemates, with landlords, with boilers breaking and not getting repaired. Like in a way it was a very kind of low-income status. And I remember kind of looking in awe at some of the PhD students who might be a little bit older who might have worked before and had a bit more savings or maybe had a partner who could support them, who lived in a real adult flat and had furniture that they bought new rather than scavenged from the streets. And to me that was very much a vision of the long-term future. It’s definitely not something I was doing then.

12:27 Emily: Did you find that it was helpful to have that comradery with some of your classmates? Did it make getting through this experience a little bit more bearable?

12:37 Lucie: Yes, and to some extent, even people who would start their first job in London. So, not a PhD student, would probably be on a similar income. And that was 2010. It was post-global financial crisis. So actually some people had decided to do a PhD or go to graduate school just to avoid getting a job. Because there were so few jobs. So that was kind of the economic climate of the time, which has improved slightly now, but we were all very much in that same mindset regardless of whether someone was starting, you know, their first teaching job or was doing your PhD or had a job in admin or in sales at a small company. None of us were making the big bucks.

Money’s Impact on Lucie’s PhD Perfomance

13:20 Emily: How do you think that being–it sounds like very consumed with thoughts about money and decisions around money on a daily basis–do you think that had any effect on your scholarship?

13:34 Lucie: Do you mean how I performed during my PhD?

13:37 Emily: Yeah. Like, let’s say your income was double of that, and you had an easier time with money, there was less stress there. Do you think that you would have done better?

13:49 Lucie: I actually think the opposite in that because I couldn’t do that much outside of going to work and coming back home, I worked really hard. And that’s what I would just do. I had a very traditional existence of cycling to Uni, doing my PhD, and coming back. And I think that to some extent doing my PhD, was a release from my money worries, and that’s why I worked so hard on it. So that could be my specific experience.

14:18 Emily: Yeah. I don’t know if that’s generalizable. I mean, I’m happy to hear that you thought it was a positive effect on your work. But I remember when I was interviewing for graduate schools that I heard that argument from–I interviewed in a city that didn’t have a whole lot going on. A very, very small city, rural–and the argument was kind of, well there’s nothing to do here except for our work. And the weather is really tough in winter. And so we just work, and that’s all. Versus if you lived in a very exciting city or one where there’s just a lot more fun activities going on, you might be more tempted to get out of the lab and go to these other things. But we’re talking about living in London and having that attitude. So, I’m a little bit surprised by that. That you were able to kind of “tunnel vision” on just your work during that time.

15:07 Lucie: Yeah. I think that in that case, it’s very much necessity is the mother invention or this dictates how you behave.

15:16 Emily: Yeah, exactly.

15:16 Lucie: And that’s why I was very relieved when I moved out of London, came to Australia where the cost of living compared to London is lower. You know, it’s kind of insane to say. Australia has a reputation for being expensive, but I found Australia very cheap.

15:32 Emily: Yeah. Let’s talk about that transition now. But first, how many years were you in London doing your PhD?

15:38 Lucie: Four years.

Financial Life as a Postdoc in Australia

15:39 Emily: Okay. So that’s plenty of time for this to become a very ingrained mindset and approach towards money. So, you finish up and you’ve accepted a postdoc in Australia. Tell us about that. Tell us about the money that you’re making and where you’re living and so forth.

15:55 Lucie: Yes. I was very excited to come to Australia to come to Melbourne. As I said, I would be making $80,000, which was way more money than I’d ever made. I could afford to live on my own, which was a big thing in a really nice little flat in the inner city. I bought a car, I bought new furniture, you know, things were going really well. But what I noticed as well was that I did keep a lot of my former habits in the sense that, for example, Melburnians are big fans of their coffee. All the postdocs would go to the really nice coffee shops and have take-away coffee and bring it back to their office while I was very purposefully making instant coffee in a little kitchen so as to avoid buying coffees. And most of my decisions were like that in that I still got reclaimed furniture from the streets. I would do most of my shopping at op shops, which is very eco-friendly but there is a limit to how healthy that is as well. And so, even though my income was higher, I had still kept that mindset of trying to keep my cost of living as low as possible. Not really from a conscious intention, but just because that was the only thing I knew how to do.

17:13 Emily: Yeah, it sounds it’s actually hearkening back to your example from your grandparents, right. Even the coffee, specifically. So this is really interesting to me to talk to you about this transition because it’s something that I think about a lot and that I talk about quite a bit as well of how should PhDs manage their money once they’re out of graduate school. And I think the standard personal finance advice that I often say as well is live like a college student. And that’s the general advice, and the way it applies for graduate students that I say is “continue at your graduate student lifestyle for as long as possible.” Even though, once you’re making this higher income, to kind of make up for the lost time and the lost income from the previous years, so that’s a time when you can be building up savings and starting to invest and so forth.

18:05 Emily: But I trip over that advice sometimes a little bit. And especially in a case like yours, because if your lifestyle was so constrained, due to your graduate income, that’s not good advice any longer, right? You should increase your lifestyle as your income goes up, and still do all the things you want to, you know, be saving and so forth, investing or paying off debt, whatever it is you need to do. But if you have been consumed and shutting out large portions of your life because of lack of money, that’s not something that should continue. So I’m really glad to have your example as one that is counter to the advice that I usually give and the advice that many people would probably hear once they are seeking out personal finance content. So, can you talk a little bit more about that change? Once your income is higher, how did you start changing how you were using your money and thinking about your money?

Money Change #1: Saving Toward Retirement

19:05 Lucie: The first decision that I ever made about my money, that was a very good decision, which was based on the advice of one of my friends who’s a financial advisor, was that when I started my postdoc in Australia, we’re very lucky that we have 17% of our salary be put into a superannuation fund by our employer. So the employer adds to our salary 17% and puts it into a fund for our retirement. But we can make additional pre-tax contributions. And I made the maximum pre-tax contribution, which was 9.5%. So, I basically had a quarter of my salary going into a super every month, and that was not increasing my lifestyle. That was making a very conscious decision about investing in my future. And that was pretty much the little seed that then grew not into expanding my lifestyle but into this view of investing in myself in the sense that I can invest in savings, I can invest in my super, but I can also invest in my own wellbeing, not because I’m being frivolous, but because it pays off.

20:17 Lucie: It pays off, let’s say to have a gym membership, to have a yoga membership, to have healthy social relationships, et cetera. And so I think that I did go to some extent through that transition of seeing not money as like an enemy or something that needs to be hoarded, but something that can be used as an investment for a good life. And that was what I’d seen in some of these older PhD students in London who were maybe buying a property, et Cetera, that they were investing in their future. Versus when I was doing my PhD, I was not future-oriented. I was in survival mode. Versus this increase in salary opened up for me the possibility that I could plan for a future.

21:01 Emily: I think you put that so well and I want everyone listening, if you’ve resonated with anything, Lucy said so far to go back a minute or two and listen to that–what you just said, over again–because I think it was so, so insightful and well-put. As you were saying, the first intentional money decision that you made after this income increase was not about just going crazy and spending because you’d been so restricted for so long and just splashing out on everything. But rather, being able to think about really changing how you even viewed money. What you said was in viewing it as being able to invest in yourself and having an enjoyable and healthy lifestyle overall rather than trying to hoard it as much as possible because there was such a scarcity, you know, before that point.

21:52 Emily: And I did want to add a slight translation for my, my listeners in the U.S. So, our equivalent to what you did was, when you got your higher salary, basically we would call it “maxed out your 401(k),” which in the U.S. is $19,000 per year. So if anyone’s listening who has started a new post-PhD job and you’re wondering what to do with that lovely salary bump, maxing out your 401(k) is an excellent thing to do. For the reasons that Lucy just mentioned, that it is an investment in yourself and it’s an investment in your future.

Commercial

22:25 Emily: Emily here for a brief interlude. Through my business, I provide seminars and webinars on personal finance for graduate students, postdocs, and other early-career PhDs for universities, institutes and conferences, associations, etc. I offer seminars that cover a wide range of personal finance topics and others that take a deep dive into the financial topics that matter most to PhDs, like taxes, investing, career transitions, and frugality. If you are interested in having me speak to your group or recommending me to a potential host, you can find more information and ways to contact me at pfforphds.com/speaking. That’s p f f o r p h d s.com/speaking. Now back to the interview.

Money Change #2: Impulse Shopping

23:13 Emily: So were there any other changes that you made, after that point, after starting to think about the long-term with respect to retirement? What other changes did you start making?

23:24 Lucie: Probably the next change that I made, which was not a good change, and that happened in my second postdoc, was that I started to impulse shop, and that was entirely related to the stress that I was under. So for, as you said, for a few years I managed to keep my spending quite low, and to have that fairly frugal lifestyle. But then after years of PhD, years of postdoc being put under a lot of pressure, I was starting to struggle, and I could see that being reflected in my spending. And I very quickly knew that this was an issue. So it wasn’t that I was being frivolous in being released, I was using that kind of as an emotional Band-Aid. And that kind of was one of the alarm bells that told me that maybe I need a bit of time off or to think about why I was in academia and what I’d wanted to do. Because one of the symptoms of this was how I was sending my money, which was not really in accordance with my values, and that was quite troublesome to me.

24:31 Emily: Yeah. I think that’s also very common behavior, whether people can afford it or not. So, coming to impulse spending just to emotionally relieve some kind of stress or difficulty or pain that’s going on. So, yeah. Can you tell me more about, having recognized that issue, what then did you do? You just mentioned you took some time off from your postdoc.

Leave of Absence from Postdoc

24:56 Lucie: So I think this was kind of part of a larger quarter-life crisis in the sense that the pressure had been mounting probably since the first day that I started my first postdoc in Australia. And now that was three years later of full-time work with a lot of international travel, a lot of publications. We’re all familiar with that kind of lifestyle. And I just didn’t know why I was in research anymore. I felt really lost and kind of, as we talked about before, I could not see my future in it. And I didn’t know if it was because I was too stressed or confused or because it was genuinely not what I wanted to do. So I was very lucky that I could ask for a six-month unpaid leave of absence from my university and kind of take a little break from all my responsibilities. Because, especially in my first postdoc, I think I must have supervised four or five students to completion. I think I kind of bumped to a lecturer role very quickly. But that amount of responsibility, and then it kind of caught up with me a few years later, was like, well, I’m going down this route very quickly. Do I want to continue with this route?

26:16 Emily: Yeah, really in many jobs, many workplaces, there is a great deal of just going with the flow and some inertia. And you can get to a point where your job duties are not at all kind of what you expected or what you signed up for, but it evolved. So that’s amazing that you made the decision and also were able to say, “okay, hold on a second, I need to take some time to figure out where I really want to go next.” And this is maybe a little bit of a naive question, but were you able to fund that period of being away from your job because your expenses had been so far below your income for the previous years?

26:53 Lucie: Yes, I had a lot of savings at that point.

26:56 Emily: Yeah. And, what I say quite a bit, that money gives you options. And so, you’d been earning quite a lot and saving quite a lot for those few years, and then you had the option to take a step back and have that time to reevaluate. So, what did you do with that time off?

Personal and Career Development Journey

27:16 Lucie: First, I had a holiday to see my parents in Europe, which was great. And I think the first two or three months of the six-month period, I was brain dead. I was recovering. I was watching TV, doing all of these silly things that people do when they finish their PhD. But I’ve seen that quite a lot in first or second postdocs in that people who don’t take a break between their PhD and their postdoc tend to get hit at a later date with trying to cope with all that change. I had also moved to Australia by myself and so I think it just all caught up with me a little bit later. So, I spent a few months resting and relaxing, and that’s when I started to coach myself. I became very interested in these personal development and career development books.

28:09 Lucie: I started to use a career coaching book that’s called, What Color is Your Parachute? It’s a very famous career coaching book.

[* This is an affiliate link. Thank you for supporting PF for PhDs!]

28:16 Emily: Yes, I’ve read that.

Part-Time Editing, Part-Time Postdoc

28:18 Lucie: Yeah, it’s great. And basically, I figured out that probably a very good job for me, which matched to actually want I wanted to do as a child–I wanted to be a writer. And what I was enjoying, what I was really good at as an academic was publishing. And kind of putting these two things together, I was like, “well, getting a job as an editor would be quite a good fit.” And I got a small job with a big global editing company, editing research papers, writing research papers, kind of being a writer for hire. And I really enjoyed that but it paid very little, and I was just starting out. And I could see with the budgeting that I had started doing when I was off work–because that was another really great habit that I’ve gotten into–was that just having that editing job was not gonna cut it for the type of life that I wanted. And that kind of spurred that decision to go back to my postdoc part-time. I was also not sure whether I wanted to quit academia completely. I thought that maybe if I worked part-time, I could cope with the challenges of academia better because I would have reduced hours. Then I could do my editing job as well. So that was the plan in that period, which would be to do the postdoc job part-time and the editing job part-time, and then together it would make a healthy income.

29:52 Emily: I love just how intentional you were with all of those decisions. The series of decisions that you made there, in trying to align your career with what you really wanted to do. And also, you briefly mentioned, but starting to budget is a major, huge leap in one’s personal finances. And that, it sounds like, sort of contributed to the career planning. Right? How much money do I actually need to make to fund the lifestyle that I want and then how can I redirect my career to make sure that I make that amount of money? And is that how it worked out? Did you find that the half-time postdoc position was lower stress, and was that a good situation that you were then in?

Backfired Plan: Full-Time Work for Part-Time Pay

30:35 Lucie: In a way that was a complete failure, in that I was doing full-time work for part-time hours and part-time pay. And I’ve heard that story a lot with other people, in that research is a job that is difficult to do part-time. And a lot of mothers, a lot of people who would want to work part-time for lots of reasons, find it challenging. After a while, I did end up quitting the editing job because it was too much in that postdoc responsibilities would come during my editing hours and would influence the quality of my work at the editing company. And because I was an employee of the university, they kind of took it as this is your priority, and your other job is not a priority. And that was quite difficult to manage. And also at that time I would realize that having my own business would enable me to make the kind of money that I want it to make from editing instead of working for an editing company. And so that spurred my decision to quit the editing job and to start my own business. So, as you’d mentioned, some of these decisions were intentional, but also some of them were just due from the decision to go part-time, in a way, backfired.

32:02 Emily: Yeah. So, did you end up not staying part-time for very long? How long did you stay at that part-time?

Going Full-Time into Self-Employment

32:09 Lucie: I stayed part-time for a year. And then I went full-time with the business. I had a few months to start the business when I was still part-time at the university. And that gave me a little bit of a cushion. And then again with the budgeting, I realized within three months that actually with the business, I was making enough money to not need the Uni job, which I then let go of. It makes it sound like a very drastic and calculated decision. There was a lot of kind of emotional decisions that went into it as well because I love research and I continue in a way, but I knew that having my own business would be a better decision for me for the lifestyle that I want to have, for the type of people that I want to surround myself with, etc. And finances were I guess one of the drivers of that decision. But there were also lots of other things that went into it.

33:08 Emily: Yeah. I have many of the same thoughts around and motivations around becoming self-employed. So, we’re going to talk plenty about your transition to self-employment in the second part of this two-part series. But before we do that, I wanted you to introduce this Good-Better-Best framework that you started using. I believe during this period when you were taking a break from work and when you started budgeting. What is that framework, and how were you using it?

Good Better Best (GBB) Framework

33:40 Lucie: Yes. So the framework that I was using at the time along with my budgeting is called Good-Better-Best goals. And it’s a framework that was devised by business coach Megan Hale. So when I was on my break, I just sucked up a lot of books and podcasts on how to be an entrepreneur. And usually these guys have much healthier attitudes to money. People have worked really hard on their money story and their finances to be at a stage where they can own their own business. And so that GBB method relies on defining Good-Better-Best benchmarks in terms of income generation. So, your “Good” goal is your minimum viable income. It’s the minimum of amount of money that you need to survive. Probably, my income when I was a PhD in London was even below what could be called a minimum viable income because it came with so much strain.

34:40 Lucie: A “Good” goal in the GBB framework is your basics, your rent, your bills, et cetera. Your food, and maybe something that you find really important–a little bit of going out or a Netflix subscription, but it really doesn’t go overboard. It’s pretty much the minimum that you need to have a relatively happy life. Then it gets very exciting when we go to the “Better” and the “Best” goals because then we start to cast out some of these big dreams that we have. So, for example, for me and my “Better” goals, I’ve got things such as buying furniture, buying a new dog, going on holiday. So, that’s when your lifestyle starts to improve and increase. Like you were mentioning, with having a postdoc that has better pay. Usually, people get to that “Better” benchmark where they can start to save money. They can work towards these big dreams. And because they cast it out in advance, it’s very motivational in the sense that, let’s say budgeting or restricting your income and things that you don’t like. It comes natural because you want to reach these other goals. Instead of feeling restricted, you’re just moving your money around to enable going towards the things you really want.

35:56 Lucie: And then the “Best” goal really blows your mind in the sense that if you could make that much money, it would be almost unfathomable. And you could afford so many different things. So, here you can cast a lot of these bigger dreams like buying a house or going on very luxurious holidays, et cetera. And so because you have these three benchmarks, you can always assess where you are in this very logical and objective manner. And maybe that’s something we’ll go into the next episode. It helps you get out of this very emotional attitude to money or this very fear-based attitude to money because then they just become numbers in a spreadsheet. They are in an order: Good, Better, Best. And then you can address them in this objective manner rather than having no numbers or this nebulous idea in your head that your dreams are never going to come true because they are too expensive, versus when you know exactly how much it’s going to cost, you can start working towards it.

Expanding the GBB Framework for Personal Goals

36:59 Emily: Yeah. I think you explained that very well. So, the source that it came from for you and the way that you first learned about it is very oriented around being self-employed or being a business owner in terms of having variable levels of income and a degree of control over your income. If I make this amount that’s going to keep the lights on and my life’s going to be okay. If I strive for this amount, then the next levels I could unlock in my lifestyle, and then, okay, the third level is even well above that. But given your history, coming as a PhD student and then as a postdoc, how did you massage this framework into something that you could use maybe in your personal life and not just as an aspiring business owner?

37:46 Lucie: Yes. Well, first, just defining the “Good” goal. This is applicable to anyone in the sense that most people actually don’t know their minimum viable income. And that would change their decisions on what type of job to take, what city to move to. They might think that a certain city is too expensive or a certain job doesn’t pay enough, et cetera, versus if you have a really good handle on how much you actually spend. For me, I’ve done personal budgeting for more than a year, so I know my yearly fluctuations. That enables me to make much more informed decisions about every aspect of my life. Because if I want to go for job, let’s say I’m not self-employed, I would know what this job would allow me to do and whether, let’s say I would be ready to move to a cheaper area or to a more expensive area. And the GBB goals would put that into context.

Financially Navigating a PhD Career Transition

38:47 Emily: Yeah. I actually love that you brought that up in terms of evaluating your next position. If you’re getting out of graduate school, going to a postdoc, going to another job. This is actually something that I’ve talked about in some materials that I released in the summer of 2019, which if you want to check that out, you can go to pfforphds.com/next. N e x t. And that’s about putting a job offer, a salary offer that you receive in the context of the local cost of living for the new place that you don’t live yet. And there’s ways to do that without having tracked your own spending like you’re talking about. Like trying to figure out, okay, how does this new city’s cost of living compare to where I currently live, what I currently make, what would I be making there? How does it compare?

39:27 Emily: But it’s much, much more powerful if you actually do what you’re talking about and have tracked and budgeted for yourself wherever you’re currently living. And it gives you so much more information for then evaluating that next salary offer. And like you were saying, okay, maybe in graduate school, you’re able to spend at the “Good” level. Or maybe you’re not. Maybe you’re at an insufficient level and it’s even below what you would consider to be a “Good” level of spending. You’ll at least have a handle on that. You’ll know where your current salary and current expenditures relate to that, “Good” or “Better” or whatever it is level. And that will help you evaluate, as you were saying, the next position that you might be offered. Or in your case, well, how much money do I really need to make to make this leap into self-employment, which will be so much better for me and you know, x, y, z other areas. But can I do it financially? It helps you evaluate that. Am I getting that right?

40:21 Lucie: Yes. Completely.

Final Advice for a Healthier Money Mindset

40:23 Emily: So, something that you mentioned when we were first talking about doing this interview was that you had used this GBB framework to heal your mindset towards money. So, that’s this period that we’ve been talking about. And when you’re really facing your numbers and starting to budget and so forth. What advice do you have for another, let’s say PhD student currently who is struggling both with a low income and with an unhealthy mindset towards money?

40:53 Lucie: Yeah. My main advice would be to start taking action now in the sense of doing very basic budgeting because not knowing where your money’s at makes things worse. We think when we’re putting our head in the sand that things are better because we’re not looking under the hood but it actually makes things worse. And the reason why it’s important to take some form of action really early on–and this thinking is corroborated by forms of therapy such as cognitive behavioral therapy–is that by changing your behaviors, you actually change your beliefs. It doesn’t really work the other way around. You won’t wake up tomorrow with another set of beliefs about money. It’s about taking action. And then this informs our beliefs and how we evolve in relation to money. And so by taking small actions such as when I started, which was very simple, which was just to print out my bank statement and then put a little circle around the expenses that brought me a lot of joy or a lot of value and then a little cross with the ones that I was not so sure about. I was like, maybe that’s wasted money. And then just gradually adjust your spending so that you only have the little circles. And that can help you towards what is your minimum viable income, what’s your “Good” goal without all the extraneous bits that you spend money on but actually you don’t enjoy that much.

42:14 Emily: Yeah, I absolutely love that advice. It’s sort of increasing the efficiency of the use of your money. So, I think that’s wonderful advice for that student.

Outtro

42:23 Emily: Listeners, thank you so much for joining me for this episode. Pfforphds.com/podcast is the hub for the Personal Finance for PhDs podcast. There, you can find links to all the episode show notes, a form to volunteer to be interviewed, and a way to join the mailing list. I’d love for you to check it out and get more involved. If you want to support the show and my business, please go to pfforphds.com/helpout. There are plenty of ways to do so without laying out any of your own money. See you in the next episode! And remember, you don’t have to have a PhD to succeed with personal finance, but it doesn’t hurt. The music is Stages of Awakening by Podington Bear from the free music archive and is shared under CC by NC.