This post is by Tiffany, a PhD student at Harvard University.

As an undergraduate, my parents pushed for me to become a pharmacist. They had good reason to: I had good grades and loved biology and chemistry. However, after volunteering in a lab, I decided I wanted to become a scientist. My dad was initially against this decision: he made many “personal finance” arguments against it. He warned me about the long hours and comparatively low pay to other advanced degrees, and shared articles about the current “glut of Ph.D.s”. He was worried I wouldn’t be able to find a stable job. He argued that as a pharmacist, I would have a stable, high paying salary (though this is now disputed as well). My undergraduate adviser gave similar advice, “You will not make much money if you go into science: the job market is also tricky depending on what you want. Take your time to decide what you want to do.” I thought about these arguments throughout undergrad and during my two years as a technician. In the end, I decided to go to graduate school anyways.

Their arguments have given me a strong motivation to save as much as possible for the future. First, it is uncertain what will happen after I graduate. Most biology PhDs continue on to work as postdocs, but the starting salary for a postdoctoral fellow based on the NIH guidelines is only $42,840/year. I could move into other fields outside of academia; however, unlike academia, there is no clear map on how to get training and experience for these “alternative careers” outside your dissertation work. Second, compounding works better if I start saving earlier. Any money I put into investments now will likely do more for me later on in life. Unfortunately, scientists are at a disadvantage since their earning power does not increase substantially until after graduate school and postdoctoral fellowships. By then, a scientist is likely into their 30s. Unfortunately, many major expenses – such as weddings, cars, homes, and kids – rack up during your 20s and 30s.

Below, I’ve tried to illustrate these points using my brother and me as an example.

My brother graduated is an engineer. He currently makes $58,700/year in Alabama. His after tax take-home pay is $3800/month. He manages to put away ~$1500/month into his investment accounts. I started my PhD in 2012 and get $36,800/year for my stipend in Boston, Massachusetts. My after tax take-home pay is $2300/month. I manage to put away ~$600/month into my investment accounts. Assuming that no major life events happen, we can calculate how much our income, savings, and investment accounts will turn out.

In the below chart, I’ve assumed that:

For the engineer:

- He will consistently get a 10% raise every 4 years.

- He will consistently save about $1500*12/$58700 ~ 30% of his salary.

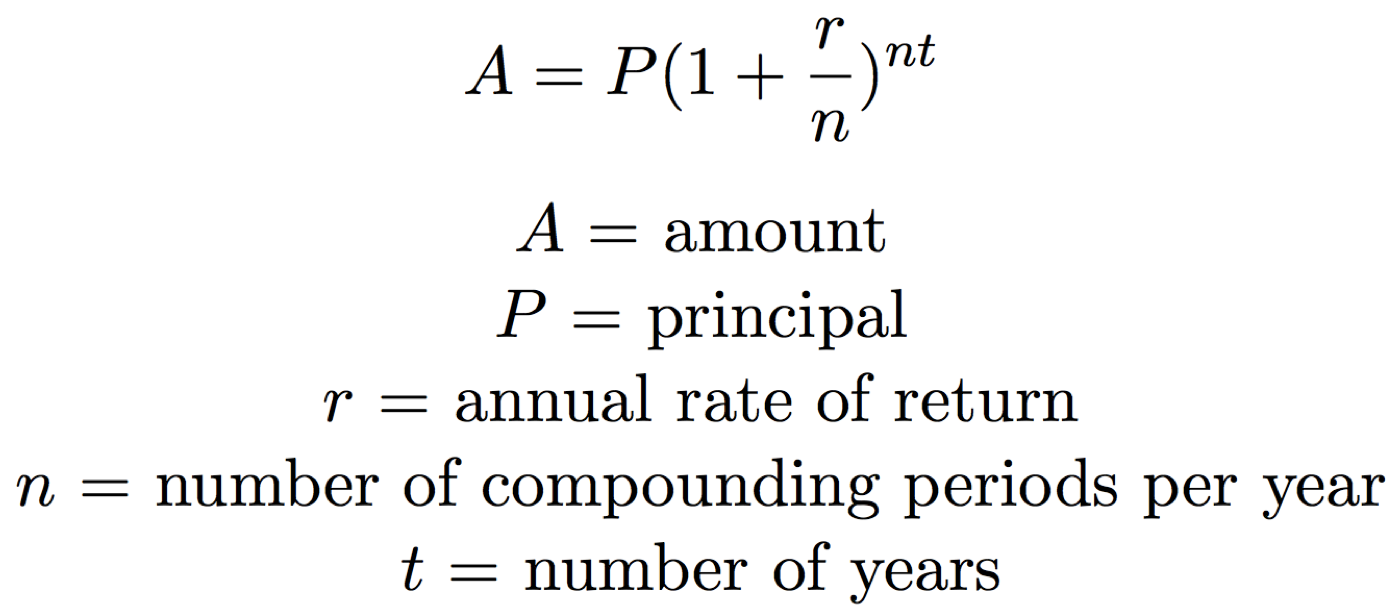

- All of these savings will compound at 7% annually, using the formula FV = P(1 + r)y, where y = # of years it compounds, P = the amount saved that year, and r = rate (7%), and FV = future value at age 65.

For the tenure track scientist:

- I am using my graduate stipend as the PhD student’s salary.

- Savings as a graduate student and postdoc will be roughly $600*12/$37,000 ~ 20% of her salary, which is what I try to save now.

- Once the scientist reaches assistant/associated/tenure professorship, she will save ~30% of her salary.

- All of these savings will compound at 7% annually.

Please note that these numbers are based off myself and my brother. They also do not take into account major life events or raises or changes in investment portfolio. Please also note that I am NOT a financial adviser and that you should seek a professional for financial advice. This article is based purely on my personal experience and hypothetical projections.

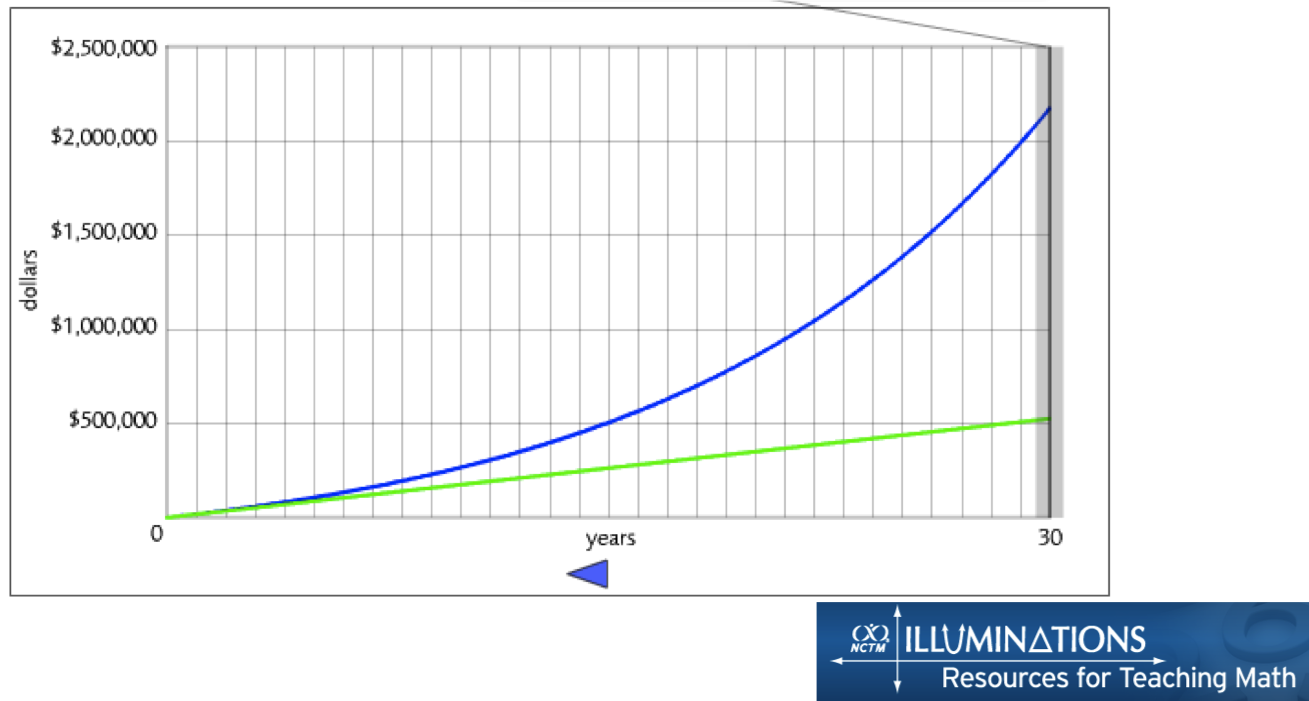

Looking at the charts above, you can see that the scientist makes about 1 million dollars less in a lifetime, but by saving aggressively, only saves $350,000 less. Still, the largest difference is in the amount compounded by age 65. The $1500/month that the engineer puts away in the first 4 years of his career can potentially become over $1 million by age 65 if the annual rate of return is 7%. Although the engineer consistently saves 30% of income, the amounts saved later in life do not yield as much. In contrast, the scientist cannot put away $1500/month until she is 32, after she has finished her postdoctoral fellowship. Her salary grows much more slowly than the engineer’s: she cannot afford to put more away until later. This results in this difference: although the engineer and the scientist have only a $350,000 in total savings, they have a $2.4 million dollar difference in what is compounded. It’s this point that makes me want to save as much as possible now!