In this episode, Emily interviews Seonwoo Lee, a PhD student in electrical engineering at Georgia Tech. Seonwoo has mastered two methods to earn extra money without “working.” Emily and Seonwoo discuss in detail their experiences with garnering credit card rewards and give both beginner and advanced tips. Seonwoo also explains a 529 hack he discovered to reduce his state tax bill that is applicable in as many as 30 states. They also briefly touch on several other methods to make money without working that are readily accessible for early-career PhDs.

Links mentioned in episode

- Schedule a Personal Finance Seminar

- Volunteer as a Guest for the Podcast

- How to Money Podcast

- Doctor of Credit: Best Credit Card Sign Up Bonuses for May 2019

- Doctor of Credit: A Beginner’s Guide to Bank Account Bonuses

- Information about 529 plans

- Blog: 529s as a College Coupon by Seonwoo Lee

0:00 Introduction

1:14 Please Introduce Yourself

Seonwoo Lee is a PhD student in electrical engineering at Georgia Tech. He did his undergraduate at Cornell. He pursued a number of ways to make money without actually having a second job.

1:48 Why have you tried to make money without working?

Seonwoo says that if you do it right, you can make more money per hour than working a traditional job. He says it gives you more flexibility, since you can do as much or as little as you want.

There is some effort involved in pursuing these strategies, but it’s not as much time you would put into working if you had a second job. Additionally, some people are prevented from officially working in other capacities, either by the terms of their contract or by their student visa. The strategies they’ll talk about are probably available to any PhD student or postdoc.

3:07 What are the two topics that we’ll go into detail discussing? What are some other strategies?

Seonwoo will discuss credit card rewards as well as banking sign up bonuses. Second, he’ll talk about the 529 trick to save money on your state taxes.

Emily mentions other ways to make money without working.

- Emily has sold items when she’s moved as part of a downsizing process. She has sold items on craigslist.

- Another option is Ebates *. Here, you make purchases through the Ebates platform and you are selling your information in exchange for money.

- Emily presents short term investing in taxable accounts as an option to make money without working. She and her husband paid off student loans through mid-term investing.

- Other options are receipt apps like Ibotta, where you upload your receipts and you sell your information to get cash back.

- Also, there is the strategy of “car wrapping,” which is wrapping your car in an advertisement and you receive money based on how much you drive. Emily recommends listening to the How to Money podcast for more information on car wrapping.

* This is a referral link. If you sign up and spend $25 through Ebates, you’ll receive a $10 bonus to your account and I’ll receive a referral fee. Thank you for supporting Personal Finance for PhDs!

7:19 How do the credit card rewards and sign up bonuses work?

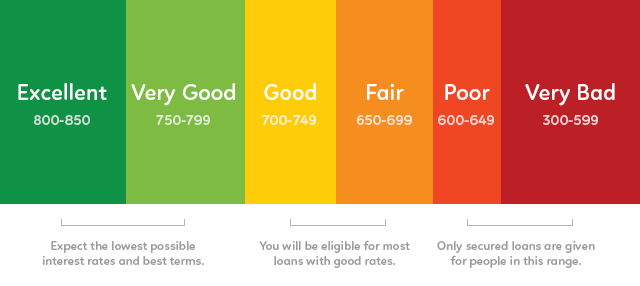

Seonwoo begins with the caveat that if you can’t manage credit cards responsibly, you should not pursue credit card rewards in any form. If you pay any interest at all when you do this, you are likely not going to reap the benefits of rewards. Emily adds that you already need a good or excellent credit score to pursue these strategies. If you carry a balance on your credit card, this strategy is not for you. Emily says make sure you are using your credit card like a debit card, and if you are you can consider this strategy.

Further reading: Perfect Use of a Credit Card

Seonwoo says that plenty of credit cards offer sign up bonuses. These require you to spend between $500 and $4,000 within the first three months of signing. The bonuses will vary from credit card points to straight cash. The offers will range from $100 to $500 in cash or 30,000 to 100,000 points. Seonwoo says there are ways to meet these minimum spending requirements without spending more than you normally would.

Emily talks about fitting these credit cards into your normal spending. She signed up for a credit card with a minimum spending requirement of $3,000 over three months. She had to put everything she was purchasing on that one card. She picked a time of year when she had to pay for car insurance and flights. She timed signing up for the credit card with when she knew she had above average expenses. Reaching the minimum spend requirements is a hurdle for people with lower income.

Seonwoo says you can see if you can pay your rent with a credit card. He says the fee may be 3%. If that is the only thing stopping you from pursuing a sign up bonus, do the math to see if the rewards are worth it. You can see if you can put tuition or fee charges on the credit card. You can see if you can pay your bills months ahead of time. He says you can buy grocery gift cards to get the charge on the credit card, but then you can spend that gift card over a longer period of time.

Emily says that someone new to this can try it with existing spending, then they can try manipulating their spending.

13:00 Is cash back or points more valuable to a graduate student?

Seonwoo says that cash back is much easier to start with and understand. There are only so many cash sign up bonuses. If you like to optimize things, credit card rewards will be more valuable if you use the rewards for travel.

Emily says that there are cards with a regular cash back rate, like 1-2% back on spending. She says that is a good way to start. Then the next level would be switching to actively pursuing credit card rewards. To make rewards lucrative, you have to be able to redeem them. She explains that in Durham, North Carolina, she couldn’t be loyal to any one airline. But in Seattle, Washington, she makes use of the Alaska Airlines credit card and its reward system.

16:18 What are the pros and cons of the annual fee situation?

Seonwoo says a lot of cards that have sign up bonuses waive the annual fee in the first year. Seonwoo’s strategy is that he signs up for the card, meets the minimum spend requirement, and by month 11 he has decided he won’t pay the annual fee and he will close the card. He says some cards are worth the annual fee, but he wouldn’t recommend keeping the annual fee card to people with lower income.

Seonwoo says that if you cancel within 30 days of being charged the fee, you can often get a refund. Ideally, set up a spreadsheet and reminders to track your credit cards.

18:54 How much money have you made using this strategy?

In his best year for strictly cash, Seonwoo has made about $2,200 to $2,500 from sign up bonuses. He says he has more credit cards and points than he knows what to do with. Most of his rewards have been in credit card points.

Emily says when she was in graduate school and pursuing cash sign up bonuses, she and her husband together made about $1,000. This can alleviate budgetary stress.

20:38 Anything else you want to add on this topic?

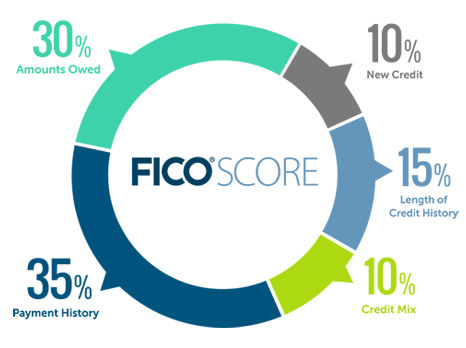

Seonwoo brings up how this affects your credit score. In general, when you apply for a credit card, there is a small hit because you have an inquiry on your report. He emphasizes that the point of your credit score is to help you get low interest rate loans or good rewards credit cards. If you’re not applying for a loan in the near future, you can use the credit score for new credit cards. He applied for cards until he started getting denied. He waited a few months, then tried again and got approved. He says people stress out a bit too much about their credit score. He says people should recognize the point of the credit score.

Emily points out that there are positive affects of having several credit cards. She also mentions some cases where you need to keep your credit score high, like when you apply for a new residence or take out a mortgage.

Further reading: How to Establish Credit in the US

24:24 How do banking sign up bonuses work?

Seonwoo says that the main difference is that instead of requiring you to spend money, banking sign up bonuses require you to already have money. You sign up for a new checking account, get a couple of direct deposits in there and keep it open for at least six months, and sometimes make some transactions. You can get between $100 or $350 for signing up for that account. Some have fees, but the bank may waive the fee for students or on other terms.

Emily mentions minimum balances, and Seonwoo clarifies that high balances requirements are usually for savings accounts. Checking accounts have minimum balance between $1500 and $3000, and the percent return is 10% to 20% in six months. This is a good option for your emergency fund.

Seonwoo recommends the blog Doctor of Credit, who has several blogs on these topics.

28:54 What is a 529? What are the benefits of it?

Seonwoo explains that there are two types of 529 plans. One is a prepaid tuition plan, which he is not talking about. The other type is an investment plan. At both the state and federal level, it is not taxed when you withdraw it for education expenses. Emily compares this to an IRA, where you are not taxed on the growth of the money if you use it for retirement. Seonwoo calls it a Roth IRA for education.

Seonwoo says 30 states and the District of Columbia offer a state income tax deduction for contributing to your 529 plan. Most states require that you have a plan with that state, but they don’t require a net contribution for the year. He says you can contribute the money to get a deduction, then pull it out to pay for your expenses.

Emily says cost of living expenses can be considered qualified education expenses for the 529 plan. She explains that you can put money into a 529, then take it out to pay rent, and then you get a state tax deduction or credit. Seonwoo says even if your living expenses are $0, you can still do this. The amount is set by the university’s financial aid office room and board estimate of the cost of attendance.

Seonwoo explains his specific example at Georgia Tech. The financial aid office lists the cost of attendance estimate for room and board as more than $10,000. In Georgia, a single taxpayer can deduct up to $2,000 of a 529 contribution. His marginal tax rate is 6%, so a deduction of $2,000 saves him $120 per year in state taxes. So, he contributes $2,000 to the 529 plan and leaves it in there for 10 days, then he takes it out. This is all it takes to get the tax deduction.

36:37 Where can we go for more resources?

Seonwoo says he learned about this by going through his state tax return to look for deductions. On his blog, he has a college tag and he has a post about the 529. The site Saving for College is a good resource for 529 plans.

Emily says this is a strategy that you need to investigate for your own state. Seonwoo mentions that there are other education credits and deductions available, but you can’t double count expenses. This 529 trick makes use of the living expenses, because this is unique to this tax benefit.

Seonwoo recommends printing to PDF the page from the financial aid office that documents the cost of attendance. This is documentation to keep if you’re audited.

40:50 Final Comments

This episode is about ways to alleviate budgetary stress by leveraging your assets and optimizing your usage of financial accounts.